Event Vendor Insurance & COI Requirements: What Venues Ask For (and How a Mobile Hat Bar Fits In)

When a venue asks for a certificate of insurance, it is rarely just a box to check. It is a screening tool, a risk-control document, and in many cases the difference between smooth load-in and a stressful email chain two days before the event.

That matters for every event vendor, from florists and DJs to branded activations and interactive guest experiences. It also matters for a mobile custom hat bar. A service like Raising the Hat Bar is creative and guest-facing, but from the venue’s point of view, it still needs to fit a familiar vendor compliance framework.

What an event vendor certificate of insurance actually means

A certificate of insurance, often called a COI, is proof that an active insurance policy exists. It usually summarizes policy dates, coverage types, limits, and the named insured. Venues ask for it so they can confirm that a vendor has the coverage required for the property, the event type, and the guest environment.

A COI is not the policy itself, and that distinction matters. If a venue requires additional insured status, primary and non-contributory wording, or a waiver of subrogation, the vendor may need endorsements that support those requests. A certificate can reflect those items, but it does not create them on its own.

This is why experienced event planners ask for vendor insurance documents early, not after the floor plan is locked and the timeline is set.

Common venue COI requirements for event vendors

Across hotels, resorts, private venues, parks, and convention centers, the same pattern appears again and again. General liability is the baseline. Then the venue adds more requirements based on the site, the event size, the load-in conditions, and the type of vendor involved.

In many cases, the first ask is simple: send a COI showing commercial general liability with acceptable limits. After that, the wording becomes more specific.

| Venue type | Common insurance asks | Typical limit pattern | Frequent wording requests |

|---|---|---|---|

| Hotel or resort | General liability, sometimes auto | $1M to $2M liability | Additional insured, exact legal entity names, primary/non-contributory |

| Convention center | General liability, auto, workers’ comp, umbrella | $1M liability, $1M auto, higher excess limits possible | Multiple additional insureds, strict certificate wording |

| Public venue or park | General liability, sometimes permit-linked coverage | Often $1M liability minimum | Government entity named exactly, event date and location listed |

| Smaller private venue | General liability, sometimes auto or workers’ comp | Often $1M liability | Certificate holder details, venue listed as additional insured |

| Alcohol-related activation | General liability plus liquor liability | Varies by venue | Liquor wording, permit review, broader indemnity terms |

After planners see a few of these requests, the pattern becomes very clear:

- General liability

- Additional insured status

- Event dates covered

- Venue listed correctly

- Submission before the deadline

Why venue insurance requirements keep getting more specific

Venues are not only worried about major incidents. They are also managing routine operational risk. A scratched floor, a trip over a power cord, damage during load-in, or a guest injury at an activation station can all become claims. The COI process helps the venue confirm that a vendor is prepared for those exposures.

Hotels and convention properties tend to be the most exacting. They often have layered ownership structures, management companies, loading dock rules, and risk teams reviewing documents. That is why a vendor may be asked to name several entities as additional insureds instead of just listing the ballroom or event space.

Public venues can be even more rigid about wording. A city, county, state agency, or federal entity may require its full legal name on the certificate and may reject a COI that looks acceptable in every other respect.

The takeaway is simple: insurance limits matter, but wording and timing matter just as much.

How a mobile hat bar fits standard event vendor insurance requirements

A mobile hat bar fits naturally into the event vendor category. It is not an unusual insurance case. It is usually treated as an experiential retail vendor with interactive guest participation, mobile equipment, and on-site setup.

That is good news, because the baseline expectations are familiar. A mobile hat bar generally does not carry the same risk profile as a mobile alcohol bar or a food vendor. There is no liquor service exposure unless alcohol is being served as part of a separate offering. There is no foodborne illness exposure tied to food prep. That lowers complexity.

Still, the risk is real and easy for venues to identify. Guests gather around the display area. Staff transport inventory and fixtures. Materials and embellishments are handled on-site. Some setups may involve adhesives or controlled heat application. All of that fits squarely inside normal venue risk review.

For a business like Raising the Hat Bar, the match is usually straightforward when the paperwork is ready and the venue requirements are requested early.

What insurance coverages a mobile hat bar may need

General liability is the core policy, but it is rarely the only one that matters. Mobile event businesses have exposures that travel with them, and a venue may ask about more than one line of coverage.

A practical insurance stack often includes the following:

- Commercial general liability: Covers third-party bodily injury and property damage tied to operations

- Product liability: Helps address claims tied to hats, accessories, or customized items

- Commercial auto or hired/non-owned auto: Relevant when vehicles are used for delivery, load-in, or staff transportation

- Workers’ compensation: Commonly required when employees are on-site

- Business property or inland marine: Protects inventory, fixtures, displays, tools, and equipment in transit or off-site

- Umbrella liability: Helpful for premium venues, large guest counts, and corporate events

For a mobile hat bar, inland marine or off-premises property coverage deserves special attention. General liability does not cover the vendor’s own hats, racks, mirrors, signage, POS equipment, or embellishment inventory if those items are damaged or stolen in transit or on location. Many small businesses learn that too late.

Auto coverage can also become a hidden issue. If the business uses a company vehicle, that is one question. If staff occasionally use personal vehicles to move supplies, that is another. Venues may not ask for the nuance, but a good broker should.

What venues may worry about with an interactive hat bar setup

Because a hat bar is hands-on, the venue may look beyond limits and ask how the station will operate on the floor. This is where insurance and operations meet.

A venue team may want reassurance on points like these:

- Load-in plan: Vehicle access, dock timing, freight path, and setup window

- Power use: Outlet access, extension cord management, and placement

- Guest flow: Queueing space, table footprint, and line control

- Material safety: Adhesives, embellishments, sharp components, and staff handling

- Heat-tool controls: Safe zones, trained staff use, and protection of venue surfaces

That kind of planning does more than satisfy a venue. It also signals professionalism. Event planners notice when a vendor can speak clearly about risk control without making the experience feel stiff or overmanaged.

Common COI mistakes that delay approval

Many vendors do have insurance, yet still run into approval problems. The gap is often administrative, not financial.

A few errors come up often:

- Wrong certificate holder

- Missing additional insured wording

- Limits below venue minimums

- Policy dates that do not cover setup and breakdown

- Last-minute requests sent to the broker

- Auto or workers’ comp omitted when the venue expects both

One of the most frustrating problems is the vague request. A client says, “The venue needs a COI,” but the actual venue requirements are not shared until days before the event. By then, endorsement turnaround can become the real issue, not the insurance itself.

How a mobile hat bar can make venue approval easier

The best approach is to build a venue-ready process instead of treating each event as a fresh scramble. This is where strong operations give a creative vendor a real edge.

A smart internal workflow usually includes a short intake form for every venue, a clear broker contact, and a checklist that gets reviewed as soon as the event is booked. That system saves time, lowers stress, and makes premium venues far easier to work with.

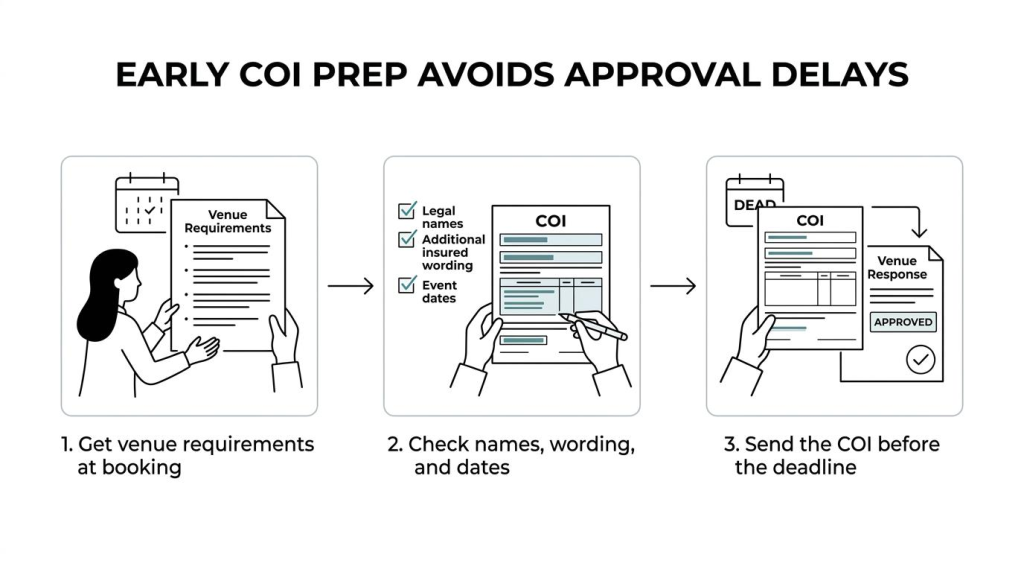

A useful pre-event process often looks like this:

- Ask for written venue insurance requirements at booking.

- Confirm legal entity names and certificate holder details.

- Check whether additional insured wording is required.

- Confirm policy dates include setup and strike.

- Send the COI well before the deadline.

- Keep a record of approved wording for repeat venues.

For event planners, this is one of the strongest signals that a vendor is ready for hotel, corporate, and convention work.

Why this matters for Las Vegas events

Las Vegas events often happen in properties that run on detailed procedures. Resorts, corporate venues, and large event spaces may have loading dock schedules, approved access points, power rules, and layered insurance requirements. A mobile vendor that arrives ready for those standards stands out immediately.

That is one reason a mobile hat bar works so well in this market. The experience is interactive, stylish, and guest-friendly, yet it can still fit into the same professional compliance structure that venues already expect. When the vendor carries the right coverage, communicates early, and sends accurate COIs, the activation feels easy to approve.

A six-step process showing how a mobile hat bar gets venue insurance approval, from requesting requirements to saving approved wording.

And that is really the goal. Not just to be insured, but to be venue-ready.